George Soros May Face a Monster Tax Bill

Deferring income helped the billionaire hedge fund manager build his fortune

George Soros likes to say the rich should pay more taxes. A substantial part of his wealth, though, comes from delaying them. While building a record as one of the world’s greatest investors, the 84-year-old billionaire used a loophole that allowed him to defer taxes on fees paid by clients and reinvest them in his fund, where they continued to grow tax-free. At the end of 2013, Soros—through Soros Fund Management—had amassed $13.3 billion through the use of deferrals, according to Irish regulatory filings by Soros.

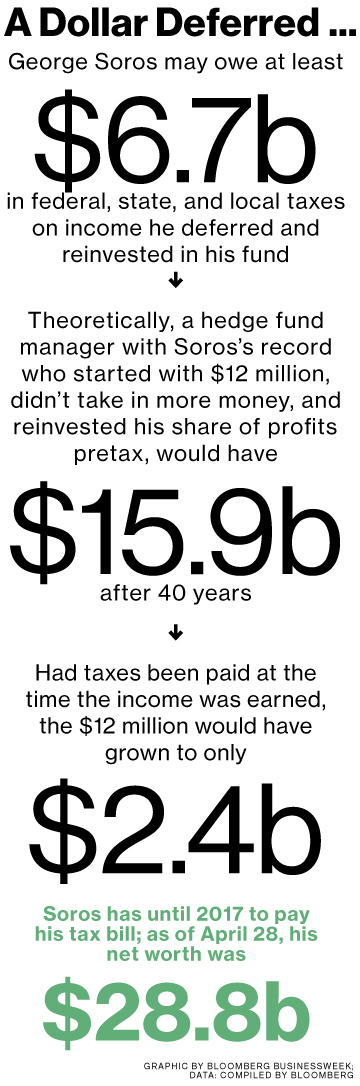

Congress closed the loophole in 2008 and ordered hedge fund managers who used it to pay the accumulated taxes by 2017. A New York-based money manager such as Soros would be subject to a federal rate of 39.6 percent, combined state and city levies totaling 12 percent, and an additional 3.8 percent tax on investment income to pay for Obamacare, according to Andrew Needham, a tax partner at Cravath, Swaine & Moore. Applying those rates to Soros’s deferred income would create a tax bill of $6.7 billion. That calculation is based on publicly available information such as the Irish regulatory filings, which provide only a partial glimpse into Soros’s finances. The actual tax bill would be affected by factors specific to the billionaire. Soros declined to comment, according to Michael Vachon, a spokesman, as did Anthony Burke, an IRS spokesman.

Just before Congress closed the loophole, Soros transferred assets to Ireland—a country seen by some at the time as a possible refuge from the law. The filings show for the first time the extent to which Soros’s almost $30 billion fortune—he ranks 23rd on the Bloomberg Billionaires Index—came from finding ways to delay taxes and reinvesting the money in his fund.

Many hedge fund managers used the tax deferral strategy, and the Congressional Joint Committee on Taxation estimated in 2008 that the new rules would generate about $25 billion in revenue for the U.S. Treasury over the ensuing decade, including $8 billion in 2017. “No person has a constitutional obligation to pay any more taxes than he is required to pay,” says James Sitrick, a tax attorney who represented Soros for decades. If Soros “couldn’t legally do it, he wouldn’t do it,” says Sitrick, who worked on international tax policy for the U.S. Department of the Treasury.

A Hungarian émigré, Soros started his career in New York City in the 1950s and gained a wide reputation for his investing prowess in 1992 by netting $1 billion with a bet that the U.K. would be forced to devalue the pound. His Quantum Endowment Fund returned an average of 20 percent annually until 2011, when he returned outside investors’ money and converted Soros Fund Management into a family office investing solely on behalf of Soros and his family members and his Open Society foundations, a worldwide network of philanthropies that promotes democracy, the rule of law, and economic advancement.

Soros started what would become the Quantum Endowment Fund in 1973 with about $12 million from investors, primarily wealthy Europeans, basing it in the then-Netherlands Antilles, according to a book he published in 1995 called Soros on Soros. He immediately began reinvesting almost all of his share of client profits, he wrote. When Soros founded his firm, nothing in U.S. law prevented money managers from postponing the acceptance of client fees and letting the money remain in their funds, where it could grow untaxed. But doing so wasn’t really an option for funds based in the U.S., because if managers didn’t take the fees, their clients wouldn’t be able to deduct them from their own taxable income.

Hedge fund managers could circumvent this obstacle by setting up parallel offshore funds for investors who weren’t subject to U.S. taxes and who therefore didn’t care whether their fund manager deferred taxes on the fees. That way, the fees—typically 2 percent of the amount invested and 20 percent of any profits—plus any investment gains, could grow without being taxed until the managers withdrew the money.

Deferring taxes is particularly valuable to hedge fund managers because most of their profits typically come from short-term trading and are subject to ordinary income taxes instead of the lower capital-gains rate. To illustrate the benefits of postponing taxes, Vyacheslav Fos, an assistant professor of finance at the University of Illinois at Urbana-Champaign, calculated that a manager with Soros’s track record who started with $12 million from investors, took 20 percent of the profits, and reinvested that money tax-free over 40 years, would end up with $15.9 billion. If that same manager paid federal, state, and local taxes on the fees and related investment gains before reinvesting them, the figure would shrink to $2.4 billion. Ordinary income taxes represent “quite a hit” to hedge fund manager profits, says Victor Fleischer, a law professor at the University of San Diego. “There is a lot at stake if they can defer that and reinvest it on a pretax basis.”

As the hedge fund industry grew, a “substantial majority” of managers obtained similar deferrals by raising money offshore, says Needham. The tactic caught the attention of Congress in 2007. Members such as Democrat Rahm Emanuel, then an Illinois representative, contrasted the ability of hedge fund managers to sock away unlimited amounts of pretax earnings with the $15,500 cap on the amount that ordinary Americans could defer through 401(k) plans at that time. On Oct. 3, 2008, President George W. Bush signed legislation closing the offshore loophole.

The law included an exemption for companies based outside the U.S. that were subject to local taxes. A week before the law was signed, Soros incorporated a new company in Ireland. Quantum Endowment transferred the deferred fees along with certain other assets and liabilities to the new company, called Quantum Endowment Ireland. Soros Fund Management never made use of the exemption to the 2008 ban on deferred fees, according to a person familiar with the firm’s finances who asked not to be identified discussing internal matters. In January 2009, the IRS issued rules that made it harder for companies to claim the exemption.

Soros set up Quantum Endowment Ireland as an Irish Section 110 company that is subject to a 25 percent corporate tax, at least in theory. Because Section 110 companies can issue so-called profit participation notes and pay out almost all their earnings as distributions to holders of the notes, they usually wind up paying very little tax.

From October 2008 through the end of 2013, Quantum Ireland paid Irish taxes of $962 on $3,851 of net income after allocating $7.2 billion of operating income to investors as distributions on profit participation notes, according to its financial statements. Most, if not all, of the notes were held by Soros’s tax-exempt Open Society foundations. Last year, Soros shut down Quantum Ireland and moved the deferred fees to a new entity incorporated in the Cayman Islands.

Soros has long called for a fairer distribution of income, once joining fellow billionaire Warren Buffett in urging Congress to raise estate taxes. In a 2011 essay, he wrote that he’d donated more than $8 billion to his foundations.

Soros might soften the potential tax blow by donating the money to the foundations, which often invest his contributions back into Quantum Endowment, according to their tax filings. That would only partially reduce the bill. Deductions for contributions to private foundations are limited to 30 percent of the donor’s adjusted gross income for the year, according to Jodi Krieger, an attorney with Kleinberg, Kaplan, Wolff & Cohen.

Soros may have found another way to defer paying taxes on fees. After Congress placed restrictions on U.S. investors in offshore funds in 1986, Soros created a security that enabled partners in his firm to defer taxes and convert ordinary income into lower-taxed capital gains, according to the person familiar with the firm’s finances. In 2010, Soros revived that maneuver by having Quantum Endowment issue $3 billion of convertible preferred partnership interests to “related parties” of Soros Fund Management, according to the Irish financial filings.

At least four tax attorneys say they know of no way for money managers to avoid the bill that comes due in 2017. “A great many people will bite the bullet and pay the tax,” says Fred Feingold, a senior partner at Feingold & Alpert. “It depends on how aggressive people are and how much they abhor paying taxes.”

The bottom line: Soros has accumulated $13.3 billion in deferred fees from hedge fund clients and investment gains on those fees.

Ed. Note: Soros is a member of The tribe.